Overview of ETA

An introduction to entrepreneurship through acquisition (“ETA”), the typical process, and the different models available to those actively pursuing the career path.

By David LaMore

April 5, 2022

Background

The term “search fund” was pioneered by Irv Grousbeck, then Harvard Business School Professor, in 1984, where newly minted MBAs would be allowed to search for, acquire, manage, and grow a business as the primary leader. In the past two decades, search funds and ETA more broadly have become a popular avenue for aspiring entrepreneurs, with there being only 20 first-time search funds in total as of 1996 and over 400 by 2020.

Although we will get into many specifics in future articles, the search fund ecosystem has primarily been dominated by MBA graduates of top-tier business schools, most notably Harvard Business School and the Stanford Graduate School of Business. Other top business schools have followed since and now offer courses on entrepreneurial acquisitions, which is how I deepened my interest at Chicago Booth. ETA has evolved and matured outside of the traditional search fund model in the past decade, with the most common alternatives being self-funded, sponsored, and incubated searches.

Many aspiring entrepreneurs and seasoned investors have moved (and stayed) in the ecosystem over the years due to the persistence of professional outcomes for searchers, financial returns for the investors, and value added to the small business community. In the popular Stanford Search Fund Primer (which I highly recommend), the report highlights that search funds generate, on average, a 32.6 percent internal rate of return (IRR) and a 5.5x multiple on invested capital (MOIC) as of the 2020 study. While the community has primarily been concentrated in the United States, ETA has become popular for international searchers in the United Kingdom, Spain, Brazil, Mexico, Chile, and many other countries.

The career path is not without its risks. Many elements of ETA have evolved in recent years due to market forces, competitive pressures from lower-middle market private equity, and the types of businesses that searchers would like to buy. These developments have made finding great companies at good prices more challenging in markets such as the US. Further, searchers must endure many sacrifices, both personally and professionally.

What is (and is not) ETA?

I like to think of ETA as the career path to entrepreneurship that does not involve launching a new business idea from a concept. Instead, it can be thought of as taking a business from one to 10 rather than from zero to one. However, in my definition of ETA, being an integral part of the search, acquisition, operating, and exit phases are necessary. Otherwise, the lines can easily get blurred with other career paths.

Some adjacent career paths are slowly being looped into ETA, but it can be pretty misleading. Most notably, CXO (“Chief Experience Officer”) programs and private equity operations roles are alternative lower-middle market opportunities for mid-career professionals who seek leadership in an organization without the search phase of ETA. Again, these programs are typically reserved for elite MBA graduates, experienced operators, and private equity professionals, but they should not be confused with a pure entrepreneurial acquisition. We will touch on these briefly for those interested, but Maverick will write content with a more entrepreneurial tint.

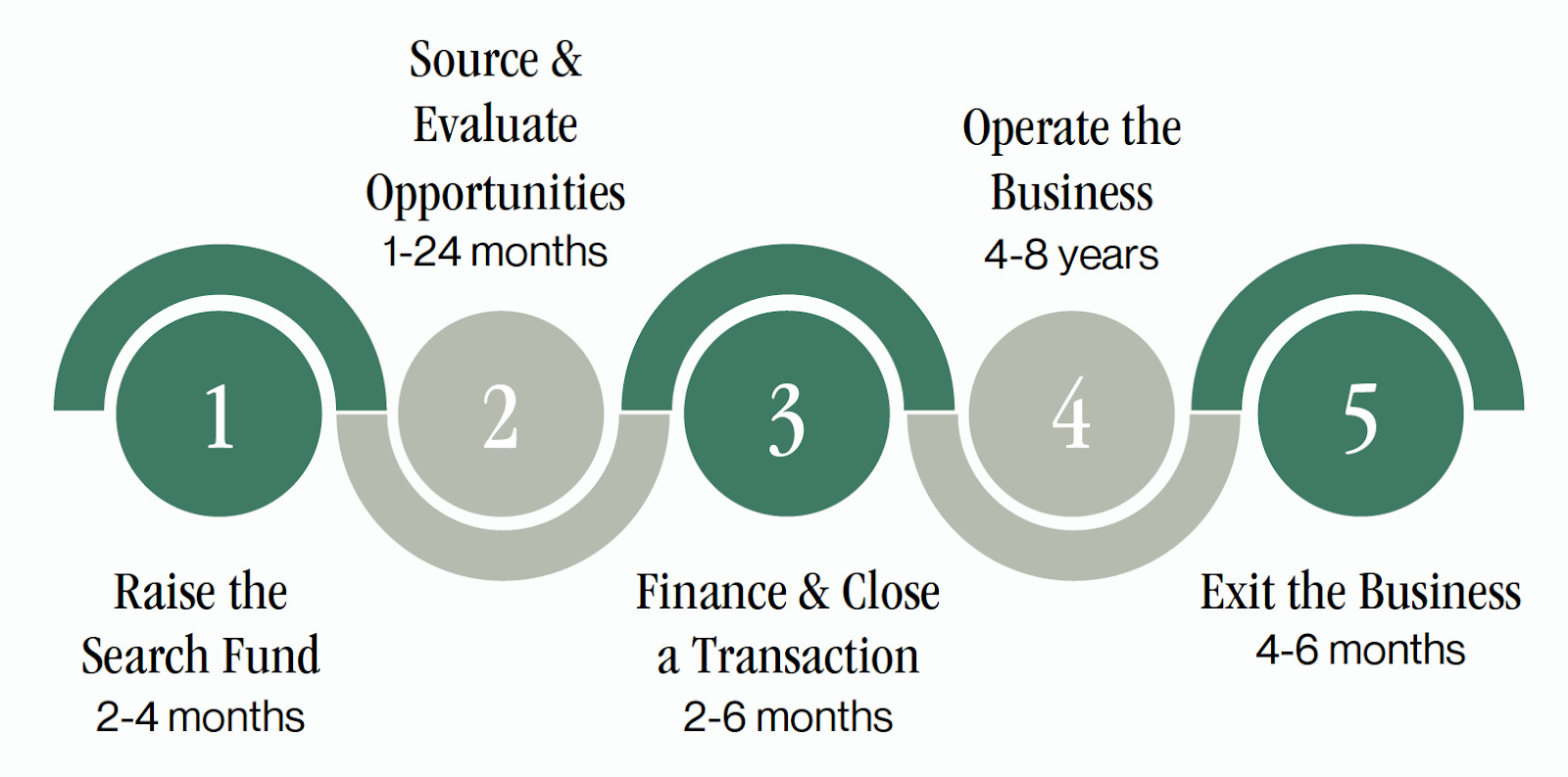

Process

Pursuing a search is not for the faint of heart. Below, the five phases of ETA walk through what one should expect and how the nature of the work differs.

Fundraising

There are four primary activities involved in raising your search fund. First, potential searchers need to network with investors to introduce themselves and get a feel for those they click with most. Second, every searcher must complete their private placement memorandum (PPM), a necessary investment document, before formal conversations regarding the capital raise. This document would include an in-depth review of your background, search strategy, fund structure, industries of interest, and more. After sending out your final PPM to investors, the third step is formally having conversations with investors and receiving commitments to your search fund. Last but not least, the searcher must partner with an attorney to complete the necessary paperwork for fund formation. Note that only Search Capital is raised at this time.

Search

Once the fund is formed, the searcher will need to set up their systems and processes to conduct outreach to business owners (through proprietary and brokered opportunities), build a website, create their email messaging campaign, craft their story, etc. The ramp-up period can be a heavy load, so I recommend that searchers complete as much of this work as possible before using their Search Capital. Once calling the capital from investors, the searcher should focus their time on sourcing and evaluating opportunities with the help of interns (a mix of MBAs and undergrads), conducting industry research, attending industry conferences, and meeting with business owners in person (when possible). The end goal is to find a business that fits the searcher’s investment criteria and where the business owner is looking to exit.

Transaction

During the search phase, searchers will have many conversations with business owners, some of them positive, and most of them will fail for one reason or another. For businesses that appear to meet the investment criteria of their fund, searchers will agree upon general price expectations and terms through an Indication of Interest (IOI) if there’s sufficient interest from both the searcher and the business owner. If conversations continue to improve after an IOI, the searcher will execute a more formal document called a Letter of Intent (LOI) with the business owner. The terms and conditions of the LOI are more specific compared to the IOI on price and deal terms and generally have a non-exclusivity clause for a particular time. Here, searchers with their investors will move into due diligence (DD), a process that involves verifying the asset you expect to be buying. We will dive into DD in a separate article more thoroughly but think of it as an all-hands-on-deck effort to ensure you’ve factored in all risks associated with the business. Finally, if all checks out in DD, the searcher and business owner will sign a purchase agreement and close the deal.

Operate

Now, the real fun begins. After closing the deal, the searcher(s) will step into key leadership roles within the company, usually the Chief Executive Officer and President. Typically there is a transition plan agreed upon between the former owner and the new search CEO, and the search CEO will aim to ramp up the business as quickly as possible. Search CEOs commonly spend the first year learning as much as possible about the company, closely working with the new board of directors, implementing the 100-day plan from their investment memorandum, and establishing a solid reputation with the company’s employees. Subsequent years will focus on larger strategic initiatives, professionalizing management and processes, and potentially further M&A.

Exit

At some point, the search CEO and its investors determine that it is the right time to exit the company. There can be several reasons for exiting the company, both personally and professionally, and in many instances, the searcher is many years in on this journey. It’s natural for many to seek liquidity, especially investors, although some search CEOs decide that they want to continue operating. The most common exit strategies are a full buyout from a financial buyer, a strategic buyout, and a recapitalization.

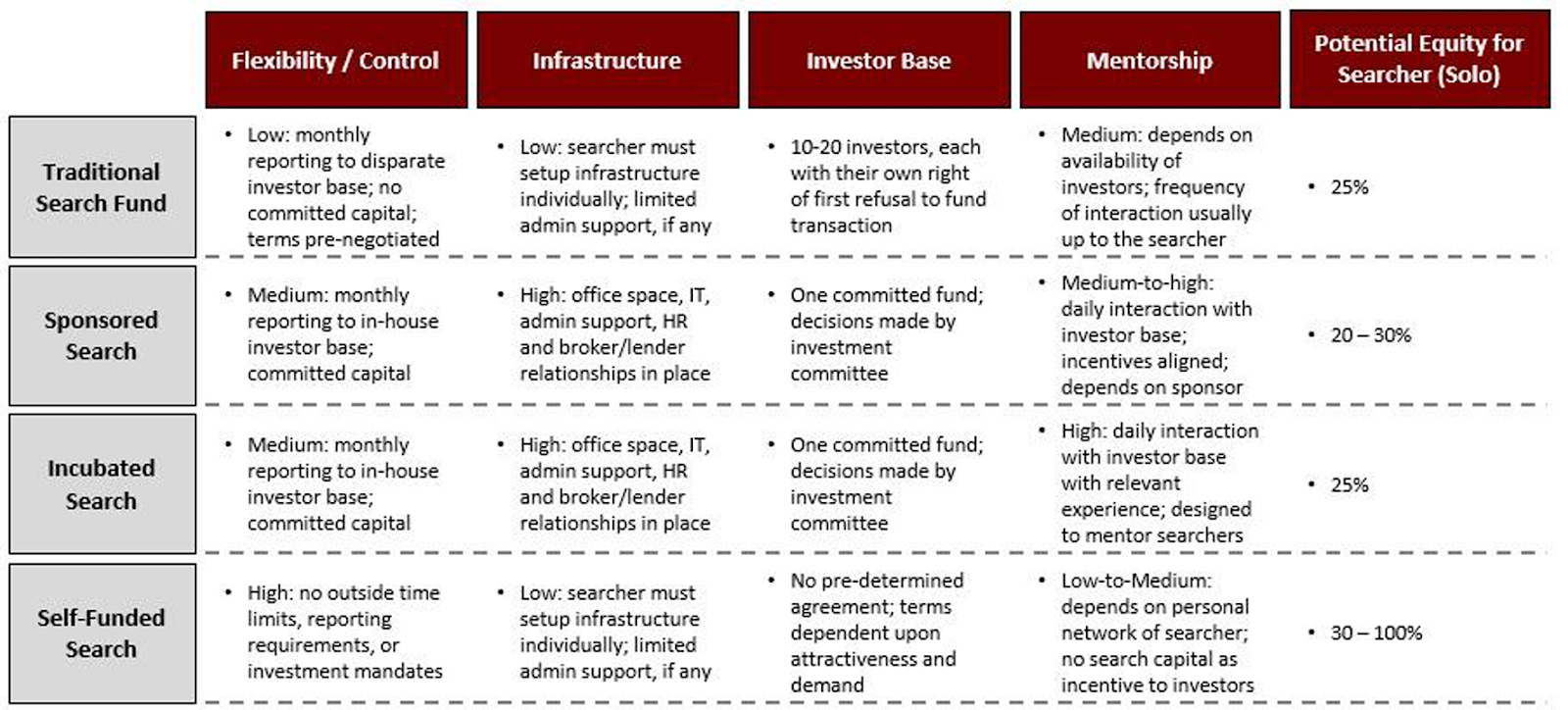

ETA Models

Now that we’ve laid the groundwork on the five phases of ETA, we can dive into the most prevalent models for aspiring entrepreneurs. Depending on many factors (i.e., one’s risk tolerance, willingness and ability to risk their capital, desire for autonomy, etc.), individuals can pursue different forms of ETA, all with a standard set of processes in an ideal world. My descriptions below will focus on the variation of the models in the fundraising, search, and acquisition phases, but please also note that there are subtle differences in later stages. Please forgive me for my brevity - now, let’s dive in.

Traditional

The Traditional path is when an entrepreneur partners with a group of investor-advisors to locate, acquire, manage, and exit a business under some set of predetermined terms. The entrepreneur can pursue this path solo or with a partner and raise two distinct rounds of capital from a group of investors.

The first round of fundraising is for Search Capital, typically ~$450,000 for a solo entrepreneur / ~$700,000 for partners to pay for the expenses (including salary), in which the entrepreneur(s) conduct a highly structured search to acquire a private company, typically up to 24 months. However, some extend into the third year if their budget permits.

Once the entrepreneur(s) come to an agreement with a business owner and their investors, they will raise Acquisition Capital. The business is typically acquired through a combination of equity financing from those who invested in the Search Capital and debt financing from small business lenders. Deal terms are highly variable and specific, and I’ve purposefully omitted many details to be discussed in future posts.

As you follow my journey with Maverick, you need to understand that I have taken the traditional path. This means that my experience will be biased towards this model, but in no way does that limit my experiences and lessons to only this path.

Self-funded

For those willing and able to risk their own capital to fund the search for a private company to acquire, the self-funded model provides the entrepreneur ultimate autonomy. The model is pretty straightforward. There is no fundraising for Search Capital since the searcher is risking their own capital, but the entrepreneur can pursue different funding sources to complete the acquisition. Some searchers will buy businesses strictly with their own capital for equity financing, while others bring in outside investors to align interests and get the deal done. Debt financing in the US for self-funded deals can vary but frequently include SBA 7(a) loans and seller notes. Anecdotally I have heard that international deals are structured with less debt given higher interest rates and more economic volatility, but it will be country and deal-specific.

An important thing to keep in mind with self-funded searches is that the deals are typically smaller than traditional, sponsored, or incubated models but provide the entrepreneur with more equity ownership and control. Where traditional search funds have the opportunity to earn up to 25% of the common equity in a business, self-funded deals can give the entrepreneur as much as 100% ownership if there is no outside equity capital.

Sponsored

Sponsored search can be a suitable model for entrepreneurs who know what they are looking for and have similar interests to one particular investor. Maybe the entrepreneur has had an existing relationship with a private equity firm that it would like to partner with for the long term. The Sponsored model is when a search fund entrepreneur partners with an investment firm, usually a family office, that is the sole source of capital for the search and acquisition phases. In return, searchers will generally earn similar economics as a traditional search while the sponsor takes a controlling interest in the firm.

Incubated

Incubated searches are relatively new and very similar to the sponsored model. The same fund structure, infrastructure, and internal support exist as in a sponsored search, but incubators exclusively invest in search fund entrepreneurs. Searchers have the luxury of working alongside other searchers daily while enjoying the same economics of the traditional search model with additional networking and competition that can be beneficial during the lonely journey. Incubators are typically reserved for solo searchers but can leverage a team of advisors and investment professionals in acquiring a business. The best examples of these firms are NextGen Growth Partners and Search Fund Accelerator.

Solo vs Partnerships

The decision to pursue ETA alone or with a partner is a highly personal and important one to make. While some entrepreneurs need a right-hand person to counter their weaknesses, others want to be in complete control of their destiny at all times. Typically, single searchers (non-self-funded) earn a higher equity percentage (up to 25%) than their partnered counterparts (up to 15% per entrepreneur), but deal size can offset the two. Historically, data from the Stanford Search Fund Primer highlights that outcomes from partnerships are better than solo searches.

When evaluating my decision to go solo, I considered my weaknesses as an individual and determined I could seek help from my investor base throughout the search and my management team during the operating phase. Simply put, for me, the risk of a failed partnership was too high since I did not have any close friends or colleagues interested in ETA at the same time and where I could confidently come to an agreement before heading down the partnership path. While we tend to hear of the successful partnerships across the entire business ecosystem, we fail to hear how many simply do not work for one reason or another. Overall I found ways to mitigate risks associated with a solo search through coursework, a summer internship, personal reflection, and simply being proactive.

To summarize

While this post may not represent all available forms of ETA, these are the most established models and ones that I would recommend for anyone considering the career path. As you may have noticed, there are structural differences that each model has that must be taken into account.

A report from Chicago Booth in 2016 nicely summarizes five of the most critical considerations across the different models: searcher flexibility, infrastructure, investor base, mentorship, and potential equity.

Deciding to pursue ETA can be a rather difficult one. It impacts not only you and your professional outcomes but also those around you - most notably your family. Some soul searching is necessary, but I hope to share many of these experiences directly with you. Much of the writings published on Maverick will directly address these topics in more detail but do not hesitate to reach out if you have questions or would like me to share something about my journey that you might find helpful.

We’ve discussed quite a bit about ETA today, so let me recap:

- The background of ETA

- What is (and is not) ETA?

- The general search fund process

- Various models available for search fund entrepreneurs

- Solo vs partnered searching

Please subscribe to stay in the loop on future Maverick posts if you’ve enjoyed this article. I encourage you to share this with just one person you know that has mentioned their desire to do something more entrepreneurial.